The nonprofit sector has a clear stake in the legislative process. From poverty to climate change to racial injustice, nonprofits work at the frontlines of the biggest problems we face today.

Nonprofits have reason to care about policies that could improve or worsen the issues affecting their communities. But what room do nonprofits have to influence legislation? Can’t you lose your tax-exempt status advocating for specific issues?

The answer is more complex than a simple yes or no.

Let’s Talk Definitions

A 501(c)(3) is a type of nonprofit organization, or public charity, that is exempt from paying federal income tax. Not all nonprofits have 501(c)(3) status. For example, labor unions, chambers of commerce, and higher learning institutions all qualify as nonprofits, although they technically have a different tax status.

In order to maintain their tax-exempt status, nonprofits have to adhere to certain rules and restrictions. One such restriction is that a nonprofit may not qualify for 501(c)(3) status “if a substantial part of its activities is attempting to influence legislation…”

What does it mean to influence legislation? Thankfully, the IRS offers guidance:

Legislation includes action by Congress, any state legislature, any local council, or similar governing body, with respect to acts, bills, resolutions, or similar items (such as legislative confirmation of appointive office), or by the public in referendum, ballot initiative, constitutional amendment, or similar procedure. It does not include actions by executive, judicial, or administrative bodies.

An organization will be regarded as attempting to influence legislation if it contacts, or urges the public to contact, members or employees of a legislative body for the purpose of proposing, supporting, or opposing legislation, or if the organization advocates the adoption or rejection of legislation.

Under this rule, these activities DO count as lobbying:

- Tracking legislation with the express purpose of influencing legislation

- Urging your supporters to email lawmakers in support of a proposed bill

- Asking the city council to oppose adding a referendum to the ballot

- Voicing support for the appointment of a particular agency leader

These activities DO NOT count as lobbying:

- Tracking legislation to understand how proposed changes could impact your work

- Meeting with a lawmaker to educate them about your work generally

- Meeting with agency staff to share feedback on an RFP or publicly funded program

- Filing a lawsuit in order to bring a controversial issue before an appellate court

For more detail about what activities qualify as “influencing legislation,” see Internal Revenue Code Subtitle D, Chapter 41, here.

How Much Lobbying is Too Much Lobbying?

To qualify for tax-exemption, 501(c)(3) nonprofits can only engage in lobbying up to an extent. There are two key tests for determining whether or not a nonprofit has crossed that line.

1) Substantial Part Test

This test assesses whether an organization’s lobbying efforts are “substantial.” According to the IRS, this is determined “on the basis of all the pertinent facts and circumstances in each case.”

If this all sounds subject to interpretation, that’s because it is. In fact, many nonprofits prefer using the Expenditure Test, because it offers a much clearer metric for how much lobbying is permissible.

2) Expenditure Test

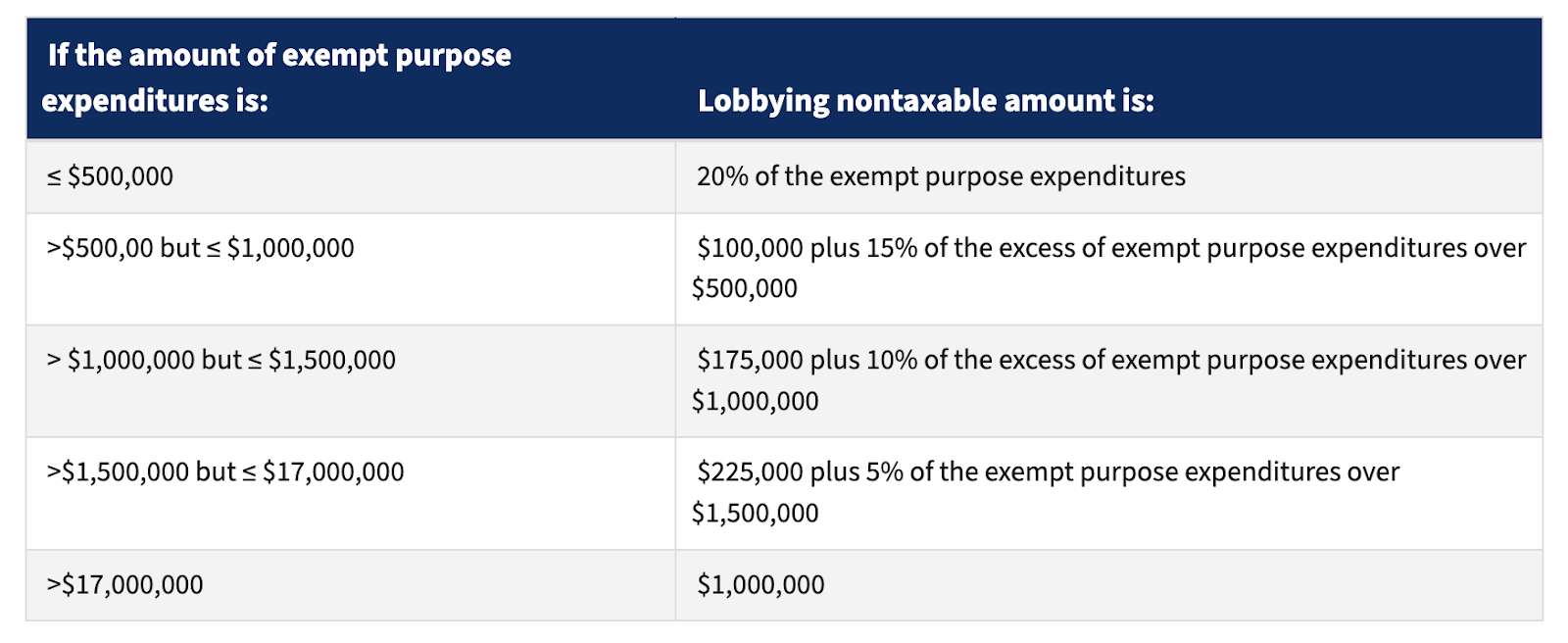

This test is based on the size of a nonprofit’s exempt purpose expenditures compared to its lobbying expenditures. For example, any 501(c)(3) with a budget of less than or equal to $500,000 can spend up to 20% of its resources lobbying. See the full chart of permissible expenditures below.

Source: https://www.irs.gov/charities-non-profits/measuring-lobbying-activity-expenditure-test

Imagine, for example, a nonprofit that spent $6,200,000 in 2024. Using the chart above, we can see that they could spend up to $225,000 plus 5% of expenditures over $1,500,000. This comes out to $460,000 that they could have spent on lobbying that year.

$6,200,000-$1,500,000 = $4,700,000

$4,700,000 * 0.05 = $235,000

$235,000 + $225,000 = $460,000

Important! In order to qualify for the Expenditure Test, a 501(c)(3) nonprofit must first file IRS Form 5768.

Resources for Staying Compliant

As a nonprofit staffer, you’re likely operating with a limited budget, a small team, and perhaps a lack of legal expertise. While these hurdles are real, there are plenty of resources to help you stay compliant while lobbying as a 501(c)(3), even without the guidance of in-house counsel.

- To start, the Internal Revenue Service offers a training series to help nonprofits maintain their 501(c)(3) status. This free video series walks you through all the 501(c)(3) basics, including required filings, prohibited political activity, and how to lobby appropriately.

- For a general overview of best practices – and common mistakes – check out the IRS resource, “How to Lose Your Tax Exempt Status Without Really Trying.”

- The National Council of Nonprofits offers numerous resources to support nonprofit organizations across the country. Check out their helpful guide on Political Campaign Activities (which are all prohibited for 501(c)(3) nonprofits) and Lobbying Activity.

Start Lobbying as a 501(c)(3) with Plural. Sign Up for a Free Consultation Today!

Disclaimer: This article is not a substitute for professional legal or tax advice.